Despite Budget Cuts, The IRS Enforcement Remains High With Automation

Over the past six years, the IRS has experienced a significant downsizing, largely due to budget cuts that reduce its resources. Many industry and news outlets have reported that cutting the IRS budget could negatively affect the IRS’ ability to enforce the nation’s tax laws. However, since the beginning of budget cuts in 2011, IRS compliance has not lost much ground. Overall enforcement revenue has remained steady, despite the IRS losing many of its enforcement personnel.

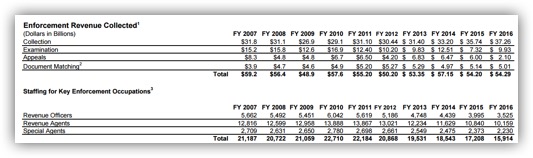

Table 1: IRS Enforcement Revenue Collected and Number of Enforcement Staff, FY2007-2016

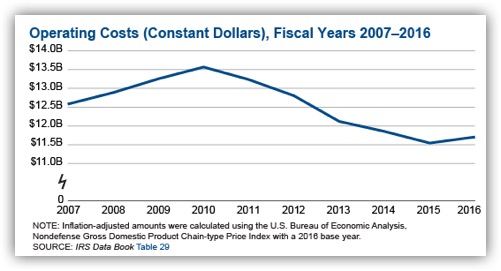

It is true that the IRS budget has taken a hit over the past six years, and future budgets continue to point to fewer resources for the IRS.

Table 2: IRS Budgeted Operating Costs, FY2007-2016

How can the IRS keep up its level of enforcement despite lower resources? It’s simple. The IRS of today is less intrusive, but more present. Here are four facts that explain:

Fact 1: The IRS collects mostly through automation.

IRS field personnel who collect back taxes and other debts to the IRS are called revenue officers. Table 1 shows 41% fewer revenue officers in 2016 – but it also shows that the IRS collected more revenue from enforcement actions in 2016 than in any of the previous 10 years. Why? One reason is a better economy, which means more taxpayers can pay their taxes. Another reason is that the IRS automates most of its collection activity through the Automated Collection System (ACS). Because ACS isn’t largely affected by the loss of revenue officers, most IRS collections don’t suffer with enforcement personnel losses.

Fact 2: The IRS has largely replaced audits with document-matching notices.

Per Table 1, IRS employees who conduct audits in IRS parlance, are called revenue agents. Since 2010, the number of IRS revenue agents has decreased by more than 26%. Revenue from audits has decreased also, pointing to the fact that the IRS has saved most audits as a last resort to police inaccurate tax returns.

Instead, the IRS has greatly increased document matching since 2001. In 2001, the IRS sent 1 million underreporter matching notices (called CP2000 notices), which flag returns that don’t match income information reported to the IRS through employers and other payers. Last year, the IRS sent 3.5 million of these notices.

Audits are expensive for the IRS and provide little coverage (only 1.3 million audits last year, or 0.8% of taxpayers) compared with more automated CP2000 notice checks, which are handled mostly by automated systems and lower-cost tax examiners.

Fact 3: IRS penalty assessments for noncompliance remain high.

Last year, the IRS issued almost 40 million penalties for late filing, late payment, and incorrect tax filings. In 2010, the IRS assessed 37 million penalties. These numbers remain high each year as the IRS uses automated techniques to correct noncompliance.

Fact 4: The IRS would rather use notices for compliance.

This is the IRS “coverage” strategy: Contact more taxpayers and they’re more likely to comply. To accomplish the strategy, the IRS issues more notices now than ever before. In 2001, the IRS issued about 30 million notices annually. Now, it is issues about 200 million annually. That is a 570% increase in notices sent, despite the number of taxpayers increasing by only about 14% during that time.

The bottom line: Less budget doesn’t mean less IRS compliance. In fact, the IRS has created many efficiencies. You can see this with more IRS compliance activity than ever before – just in a kinder and gentler manner – through computerized notices.

Whether it is a face-to-face audit or a computer-generated notice, taxpayers should stand up and take notice when they are subject to IRS compliance activity. If you think you are in over your head (which most people are when dealing with the IRS), hire a tax professional with expertise in this area. In the end, this may be the best way to avoid additional tax, penalties, interest, and grief from a tax issue.

Was this topic helpful?