IRS pandemic refund: How to claim a potential COVID-era penalty refund before July 10

Key Takeaways

- A recent court ruling may let you claim a refund if you paid COVID-era tax penalties.

- Refunds are not guaranteed due to ongoing legal action, but filing now protects your rights.

- You can file even if you’re not sure how much you paid (including the breakout of penalties vs. interest).

- You must act fast. You must submit your Form 843 electronically via your IRS Online Account—or download and complete Form 843 and mail it with a postmark before or by July 10, 2026, to preserve your claim.

- H&R Block can help you understand how to determine your eligibility and file correctly.

A recent court ruling (Kwong vs. the U.S.) may allow millions of taxpayers to claim a refund of penalties and interest paid between January 20, 2020, and July 10, 2023. While these refunds are not guaranteed due to ongoing legal action, you must act quickly to preserve your claim.

Protective claim electronic submission and mailing deadline: July 10, 2026

H&R Block is here to help you navigate this complex situation so you can file your protective claim by the July 10 deadline. We’re here to simplify this complicated process with how-to explanations and tips from our experts.

Jump to details covering:

- How to file a protective claim using Form 843

- What is the Kwong ruling?

- Who is eligible for the IRS pandemic penalty refund?

- When would refunds be paid and why are they not guaranteed?

- FAQs

How to file a protective claim using Form 843 (Two scenarios)

You’ll start by submitting Form 843 via your IRS Online Account or downloading Form 843 from the IRS. Your next steps for filing your protective claim with Form 843 depend on if you already know the amounts you paid. Using the two scenarios below, you can determine the steps you need to take to complete your form on your own and submit your protective claim before the July 10 deadline.

| Kayla | Daniel | |

|---|---|---|

| Knows she paid $500 in penalties and interest from filing late during the 2021 tax year | Not sure if he paid penalties or interest after filing and paying his 2022 taxes late | |

| Actions to take | 1. Complete Form 843 using the instructions below 2. Submit it via your IRS Online Account or postmark your completed paper from it by July 10 to file a protective claim | 1. Log into IRS Online Account to review account transcript for 2022 2. Identify line items showing failure-to-file or failure-to-pay penalties, or interest charges 3. Confirm if those amounts were paid as part of the amount paid in 2022 4. Complete Form 843 using the instructions below 5. Submit it via your IRS Online Account or postmark your completed paper from it by July 10 to file a protective claim Can’t get the details in time? Don’t worry, we’ve got instructions for this situation. Read on. |

Form 843 Instructions: Tips to help you complete your form

Complete Form 843 with your details, including the amounts you paid in penalties and interest. If your payments cover more than one tax year, you should complete a separate form for each year.

- If you know your amounts, use the steps directly below (Amounts known).

- If you don’t know how much you paid, use the second set of instructions (Amounts not known).

Review the relevant instructions below based on your situation. You can also refer to the IRS Form 843 instructions.

Amounts known instructions for Form 843

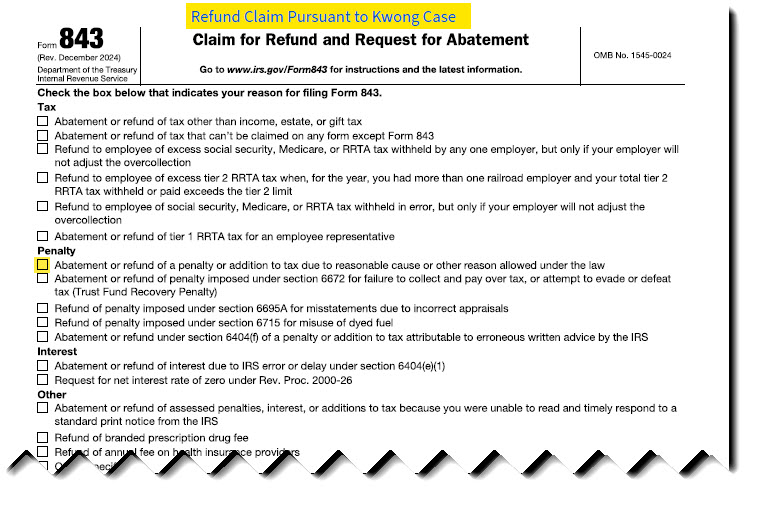

- Across the top of the form write in: Refund Claim Pursuant to Kwong Case (Click the image to the right)

- Top Checkbox section: Check Penalty – Abatement or refund of a penalty or addition to tax due to reasonable cause or other reason allowed under the law. (Click the image to the right)

- Enter taxpayer information

- Line 1: Enter tax year – For most individuals and business running on a calendar year, this will be from 01/01 to 12/31 for the relevant year. Businesses who operate on a fiscal year may have a different beginning and ending date.

- Line 2: Enter the exact total amount of penalties and interest paid (do not use “TBD”)

- Line 3: Enter actual dates of payment for penalties and interest (attach schedule if multiple payments)

- Line 4: Check ‘Income’

- Line 5: Check ‘1040’ (or applicable return type)

- Line 6: Enter IRC section as applicable: Failure-to-file penalties — IRC §6651(a)(1), Failure-to-pay penalties — IRC §6651(a)(2), Penalties for failure to make estimated tax payments—IRC §6654 (individuals), IRC §6655 (corporations)

- Line 7: Select ‘Other’ if needed

- Line 8: Include explanation referencing Kwong and requesting refund of penalties and interest already paid, including the amount claimed. You can base this on our sample language below.

- Optional attachments: If available, best practices include attaching a copy of your IRS transcript (with the relevant items identified) and copies of IRS notices or correspondence regarding the issue.

- Submit your Form 843 electronically or Mail it: If you plan to mail your form, ensure you (and your spouse if applicable) sign and date Form 843 before mailing the form to the IRS.

Sample Language for Line 8:

Filed Pursuant to Kwong

- Taxpayer requests abatement and refund of failure-to-file penalties, failure-to-pay penalties, and related interest for tax year [YEAR].

- This claim is based on IRC §7508A and the decision in Kwong v. United States, which indicates that federal tax filing and payment deadlines were automatically postponed during the COVID-19 disaster period (January 20, 2020 through July 10, 2023).

- Because the applicable deadlines were postponed, the penalties and interest assessed for this period may have been improperly applied.

This submission is a protective claim for refund to preserve the taxpayer’s rights pending final resolution of this issue.

Amounts not known instructions for Form 843

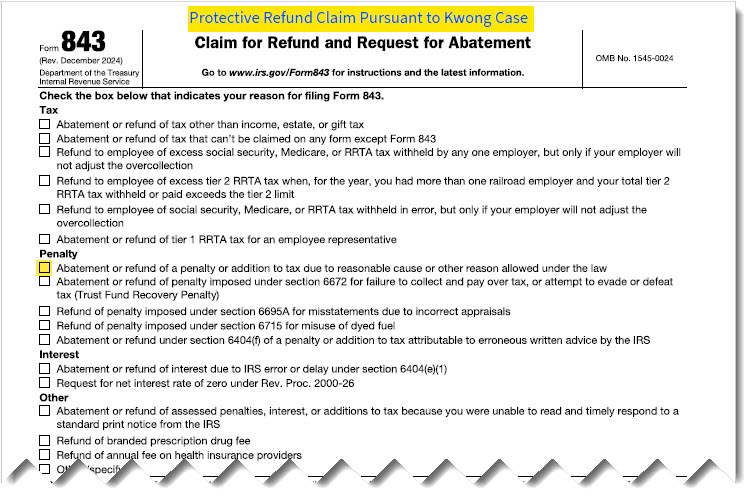

- Across the top of the form write in: Protective Refund Claim Pursuant to Kwong Case (Click the image to the right)

- Top Checkbox section: Check Penalty – Abatement or refund of a penalty or addition to tax due to reasonable cause or other reason allowed under the law. (Click the image to the right)

- Enter taxpayer information

- Line 1: Enter tax year – For most individuals and business running on a calendar year, this will be from 01/01 to 12/31 for the relevant year. Businesses who operate on a fiscal year may have a different beginning and ending date.

Line 2: Protective claim

Line 3: Leave blank

Line 4: Check ‘Income’

Line 5: Check ‘1040’ (or applicable return type)

Line 6: Leave blank

Line 7: Check ‘D – None of the above reasons apply’

Line 8: Include explanation referencing Kwong and stating this is a protective claim. You can base this on our sample language below.

- Line 1: Enter tax year – For most individuals and business running on a calendar year, this will be from 01/01 to 12/31 for the relevant year. Businesses who operate on a fiscal year may have a different beginning and ending date.

- Optional attachments: If available, best practices include attaching a copy of your IRS transcript (with the relevant items identified) and copies of IRS notices or correspondence regarding the issue.

- Submit your Form 843 electronically or Mail it: If you plan to mail your form, ensure you (and your spouse if applicable) sign and date Form 843 before mailing the form to the IRS.

Sample Language for Line 8:

Filed Pursuant to Kwong

- Taxpayer requests abatement and refund of failure-to-file penalties, failure-to-pay penalties, and related interest for tax year [YEAR].

- This claim is based on IRC §7508A and the decision in Kwong v. United States, which indicates that federal tax filing and payment deadlines were automatically postponed during the COVID-19 disaster period (January 20, 2020 through July 10, 2023).

- Because the applicable deadlines were postponed, the penalties and interest assessed for this period may have been improperly applied.

- This submission is a protective claim for refund to preserve the taxpayer’s rights pending final resolution of this issue.

We’re here to help

H&R Block’s tax experts can help you complete the necessary form and research your IRS account if needed. We can even help those who have not filed with us (fees may apply).

What is the Kwong ruling?

The Kwong v. United States ruling is a recent federal court decision that found certain IRS penalties and interest may have been incorrectly charged during the designated period (January 20, 2020-July 10, 2023).

Because of the COVID disaster, the court deemed IRS should not have considered payments from that time as late until after July 10, 2023, when the disaster period ended.

Who is eligible for the IRS pandemic penalty refund?

Individuals, businesses, estates and trusts may be eligible for an IRS pandemic penalty refund if they paid penalties or interest on payments due during the COVID-era disaster period (January 20, 2020, through July 10, 2023).

This can include:

- 1. Failure-to-file penalties

- 2. Failure-to-pay penalties

- 3. Penalties for failure to make estimated tax payments

- 4. Underpayment interest (including interest that may have started accruing earlier than it should have)

When would refunds be paid—and why are they not guaranteed?

Refund timing is uncertain. The IRS is expected to appeal against the Kwong ruling. Because of this, the IRS may hold any payments until there is a final decision.

It’s important to note that filing a protective claim by the deadline preserves your right to a refund, but it does not guarantee you’ll receive one.

IRS pandemic penalty refund FAQs

What is the IRS COVID penalty refund?

The IRS COVID penalty refund refers to a potential refund of penalties and interest paid during the COVID-era disaster period, based on a court ruling (Kwong vs. U.S.) that those charges may have been incorrectly assessed.

What penalties apply to the COVID penalty refund?

Eligible charges may include failure-to-file penalties, failure-to-pay penalties, estimated tax penalties, and related interest tied to tax deadlines during the COVID-era period.

Which tax years are included in the Kwong court case?

The ruling may impact penalties and interest tied to tax returns and payments due between January 20, 2020, and July 10, 2023, which can include tax years such as 2019 through 2022, depending on your situation.

When would the IRS pay out the COVID penalty refund?

Refund timing is uncertain. Because the IRS has appealed the ruling, payments may be delayed until there is a final court decision.

What is a protective claim?

A protective claim is a refund request filed before the deadline to preserve your right to a refund while the legal outcome is still uncertain. Filing now helps ensure you don’t miss your opportunity if the ruling is upheld.

Where do I send IRS Form 843 for refunds or abatement?

Form 843 is mailed to the IRS service center listed in the form instructions. The correct address depends on your location and the type of tax involved, so review the current IRS instructions before sending. For IRS pandemic penalty related refunds, you can also submit Form 843 via your IRS Online Account.

How do I get an IRS transcript?

You can get your transcript by logging into your IRS Online Account and selecting “View Transcripts” under your tax records. You can also request a transcript by mail if you don’t have online access.

How do I start an IRS Online Account with ID.me?

To access your IRS Online Account, you’ll need to create or sign in with an ID.me account by providing your email, verifying your identity, and following the prompts on the IRS website.

How do I file IRS Form 8821—and why would I need it?

Form 8821 lets you authorize a tax professional to review your IRS records on your behalf.

To complete it:

- Enter your name, address, and taxpayer ID

- List the tax professional or firm you’re authorizing

- Specify the tax form (for example, income tax) and the years involved

- Sign and date the form

You can file Form 8821 if you need help reviewing transcripts or preparing your refund claim but don’t want to grant full representation.

File with H&R Block to get your max refund

Was this topic helpful?