Benefits of compound interest

Key Takeaways

- Compound interest helps your savings grow faster by earning interest on both your principal and past earnings, creating a powerful snowball effect over time.

- Compound savings supports financial goals by steadily increasing your balance, helping you build emergency funds, save for purchases, and improve long-term financial stability.

- The difference between compound interest vs. simple interest becomes clearer over time, as compounding generates higher earnings by building on accumulated interest.

- The power of compound interest comes from time and consistency, allowing even small, regular contributions to grow into larger balances through repeated compounding cycles.

- Starting early and saving consistently maximizes compound interest benefits, as more time and frequent compounding boost growth and increase your total savings potential.

Building up savings is major goal for many of us. If that includes you, you’ll want to know all about compound interest. In a nutshell, compound interest is a powerful way to grow your savings over time.

One of the benefits of compound interest is that instead of earning interest only on the money you deposit (your principal), you earn interest on both your principal and the interest you’ve already accumulated.

This snowball effect can help even small, consistent contributions turn into larger balances—especially when you give your money time to grow.

How compound savings supports financial freedom

Compound savings can be one of many tools to help you build financial stability by steadily increasing your money. When your savings grow automatically through compounding, it becomes easier to build toward goals like an emergency fund, or major purchases.

Over time, this consistent growth along with consistent savings habits can help you feel more secure in your financial future.

Compound interest vs. simple interest

Simple interest is calculated only on the deposits you make, while compound interest builds on both your deposits and the interest earned over time. This difference becomes more noticeable the longer your money stays invested or saved.

| Simple interest | Compound interest | |

|---|---|---|

| What does the calculation include? | Deposits only | Deposits and interest previously earned |

In the next section, we’ll look at an example that outlines compound interest vs. simple interest.

How compound interest compares to simple interest over time

Over time, you can see the impact of compound interest compared to simple interest in the fact that you’ll be earning more (assuming all other factors are equal). At first, it may not seem like a lot—but that’s where time makes the difference. The more time you give it, the more your growth accelerates because each period builds on past gains.

Simple interest: 5% on $1000

| Period | Principal | Simple Interest | Ending Balance |

|---|---|---|---|

| 1 | $1,000 | 5% of $1000 = $50 | $1,050 |

| 2 | $1,000 | 5% of $1000 = $50 | $1,100 |

| 3 | $1,000 | 5% of $1000 = $50 | $1,150 |

Compound interest 5% on $1000

| Period | Compound Interest | Ending Balance | |

|---|---|---|---|

| 1 | $1,000 | 5% of $1000 = $50 | $1,050 |

| 2 | $1,050 | 5% of $1,050 = $52.50 | $1,102.50 |

| 3 | $1,102.50 | 5% of $1,102.50 = $55.12 | $1,157.62 |

Why compound interest is important

Understanding compound interest can help you make smarter decisions for your savings. When it’s time to choose an account type for your money, having a grasp of some of the basics can help you take that step more confidently.

Power of compound interest

The power of compound interest comes from its ability to multiply your savings without additional effort on your part. The additional savings that compounding interest generates is built-in to the process.

Over time, this creates a compounding cycle where your earnings generate even more earnings—helping your savings grow faster than with simple interest.

Spruce Savings offers 3.50%* APY–over 7x the national average.**

**The Annual Percentage Yield (APY) is accurate as of 6/19/26. This rate is variable and can change without notice. Spruce Savings Accounts prior to July 17, 2025 may be required to opt in through the Spruce app or at sprucemoney.com to start earning interest.

**FDIC average national savings as of 6/19/26.

Compound interest examples

Seeing compound interest in action can make it easier to understand how it works in real life. Each time interest is added to your balance, future interest is calculated on the new, higher amount. Over several years, this compounding effect can lead to a significant bump in your savings.

Using our previous hypothetical accounts from above, we can show how savings grow with compound interest. Let’s say that you’re saving for a house down payment over three years. You start with $500 and then are saving $500 a month for three years and can earn 5% interest on your savings. At the end of the period, you will have an additional $1,382 based on the interest compounding!

How compounding frequency affects savings growth

Simply put, the more frequent interest compounds, the faster your savings can grow because the interest is added to balance more often. Essentially, every time your interest compounds you have more money working for you.

Compounding frequency is one of those down-in-the-weeds details that helps you follow the math behind the scenes.

How often does compound interest compound?

Interest may compound daily, monthly, quarterly, or annually depending on the account. It’s not one-size-fits-all, which is why it’s helpful to check the fine print.

Daily compound interest vs. monthly compound interest

With daily compounding, interest is calculated every day, allowing your money to grow more quickly.

With monthly compounding, interest is generally calculated at the end of each month. The difference between daily and monthly compound interest becomes more noticeable over longer periods.

Why starting early increases compound growth

Time is one of the biggest factors in how much your savings can grow. Starting early allows your money to go through more compounding cycles, which can significantly increase your total balance—even if your contributions are smaller.

Waiting longer to start typically means you’ll need to save more to reach the same goal.

Pros and cons of compound interest

While there are many advantages, it’s also helpful to understand the trade-offs.

- Pros of compound interest: It accelerates savings growth over time and rewards early and consistent saving habits.

- Cons of compound interest: Growth can take time to become noticeable, so it requires consistency and patience. It’s also good to keep in mind that accounts can be impacted by changing interest rates, and lower rates can mean slower growth.

File with H&R Block to get your max refund

How compound interest supports long-term savings goals

Compound interest plays a key role in helping you reach long-term savings goals by supercharging your progress. In the early years, much of your growth may come from your deposits. As time goes on, accumulated interest plays a larger role in boosting your savings.

Just think of the snowball analogy. Like the snowball rolling downhill, your money is growing with every rotation (compounding period) and every year.

How compound interest rewards consistent saving habits

Making regular contributions—even small ones—can have a big impact over time. We’ve talked about how compound interest builds on previous earnings. That’s great, but consistent savings increases the pool of money working for you, helping you make even larger strides towards your goals.

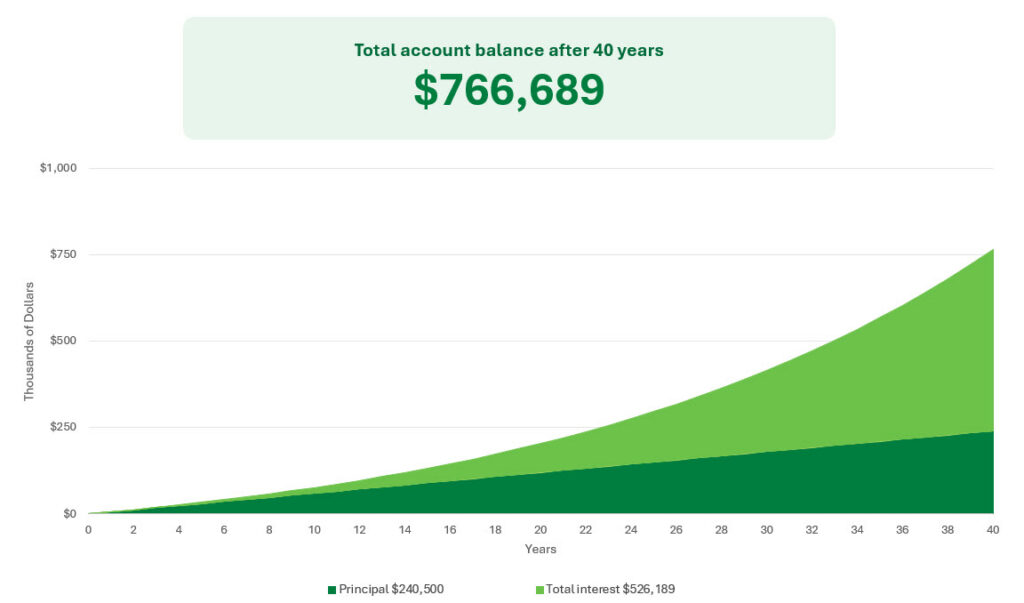

How compound interest helps build wealth

One of the biggest compound interest benefits is its ability to build wealth gradually without requiring large upfront deposits. As your balance grows, so do your potential earnings.

Over time, this can create a cycle of growth that helps you reach long-term financial milestones, such as retirement savings, more efficiently. Keep in mind that other important levers for building wealth are the interest rate and what you’re contributing to the account—how much and how often.

Using our previous hypothetical accounts from above, we can show how compound interest builds wealth. Let’s say that you are also saving for your future retirement. You are 25 when you start saving and you plan to retire when you are 65 (40 years). You start with $500 and then deposit $500 a month during this time and can earn 5% interest on your savings. At the end of the period, you will have an additional $525,189 based on the interest compounding!

How to maximize compound interest

If you’re looking for ways to maximize compound interest, here are a few strategies to consider:

- Identify what you’re saving for and what your goal amount is. Earmarking money for a specific purpose can help you resist the temptation to use savings for everyday spending.

- Start saving early to give your money more time to grow. Ideally, the more months and years you can carve out the better. But if you’re getting started late, that’s OK. The important thing is to just start.

- Contribute consistently to increase your balance over time. Creating a habit of saving—even if the amounts are small to start.

- Automate transfers and deposits to go directly into your account so you “pay yourself first.” This strategy ensures that saving is prioritized vs. just saving whatever is left at the end of the month.

- Choose accounts with higher interest rates when possible and look for frequent compounding schedules (such as daily or monthly).

- Avoid withdrawing funds for impulse spending. After your account builds up, you might be tempted to splurge. There’s definitely a place for treating yourself but dipping into your savings can interrupt growth and derail your long-term goals. To avoid the temptation to splurge, you could always consider a separate savings goal for “fun” money. Together, these approaches can help you make the most of the benefits of compound interest and build stronger long-term savings.

Compound interest FAQs

What are the benefits of compound interest?

Compound interest helps your money grow faster by earning interest on both your original balance and previously earned interest. Over time, this creates a snowball effect that can significantly increase your savings.

What is the difference between compound interest and simple interest?

Simple interest is calculated only on your original balance, while compound interest includes both your balance and accumulated interest. This allows compound interest to grow faster over time.

What are examples of compound interest?

Common examples include savings accounts Money Market accounts, and certificates of deposit (CDs). These accounts allow interest to build on itself over time.

Is daily compound interest better than monthly compound interest?

Daily compounding can result in slightly higher earnings because interest is added more frequently. However, the difference is usually small although more noticeable over time.

What factors affect compound interest growth?

Growth depends on your interest rate, how long you save, how much you contribute and to some degree how often interest compounds. Together, these factors determine how quickly your balance increases.

How to calculate compound interest growth?

You can calculate compound interest using this formula: A = P (1 + r / n) ^ (n × t)

- A is the total amount

- P is your starting balance

- r is the annual interest rate

- n is how often interest compounds per year

- t is the number of years

For example, if you deposit $1,000 at a 5% annual rate compounded monthly:

- After 3 months:

A = 1000 × (1 + 0.05 / 12)^(12 × 0.25) ≈ $1,012.55 - After 3 years:

A = 1000 × (1 + 0.05 / 12)^(12 × 3) ≈ $1,161.62

What types of accounts use compound interest?

Many financial accounts use compound interest, including savings accounts, money market accounts, CDs, and retirement or investment accounts. These accounts reinvest earnings automatically.

How does compound interest work with recurring deposits?

Each new deposit increases your total balance, which means more money earning interest. Over time, both your contributions and accumulated interest continue to grow together.

How does inflation impact compound interest growth?

Inflation can reduce your real earnings by decreasing the purchasing power of your savings. Even if your balance grows, rising costs may limit how much that growth is worth over time.

Why is compounding more effective over longer periods?

Compounding becomes more powerful with time because interest continues to build on itself each period. Longer timelines allow more compounding cycles, leading to faster overall growth.

Was this topic helpful?