New Tax Law Effective Date

Editor’s Note: This article was originally published on August 09, 2018.

On December 22, 2017, the federal tax reform bill was signed into law. While some of the provisions became effective in tax year 2017, most individual provisions go into effect in tax year 2018. A few provisions don’t go into effect until tax year 2019.

Due to the different timelines, the question “when does take reform take effect” becomes a bit more complicated to answer. Find out which provisions take effect in tax year 2017, 2018 and 2019 so you know how tax reform will fully affect your taxes.

Which Provisions Became Effective in Tax Year 2017?

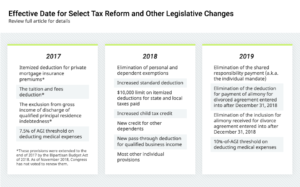

Several temporary tax benefits were retroactively extended to allow taxpayers to claim them on their 2017 federal income tax returns. For these benefits, tax reform and other legislation affected your 2017 taxes, but cannot be claimed on your 2018 return unless Congress decides to extend them. The most popular of these benefits include:

- The itemized deduction for private mortgage insurance premiums

- The tuition and fees deduction

- The exclusion from gross income of discharge of qualified principal residence indebtedness

Additionally, the AGI threshold for the medical expense deduction decreased to 7.5% (from 10%) for tax years 2017 and 2018. Bonus depreciation was increased to 100% of the cost of qualified property acquired and placed in service after September 27, 2017. Tax reform affected your 2017 taxes for these items as well, so you may want to find a tax pro in case you want to amend your prior-year return.

Which Provisions Went into Effect in Tax Year 2018?

In most cases, the answer to the question “when does tax reform go into effect” is tax year 2018. The provisions with the broadest impact include:

- Elimination of personal and dependent exemptions

- Increased standard deduction

- $10,000 limit on itemized deductions for state and local taxes paid

- Increased child tax credit

- New credit for other dependents

- New pass-through deduction, often called the QBI deduction for self-employed individuals, partners, and S-corporation shareholders

- New withholding tables applied by most employers, which generally reduced the amount of federal income tax withheld from employee’s paychecks

- Elimination of the deduction for unreimbursed employee business expenses

- Elimination of the deduction for moving expenses (narrow exception for certain military-related moves)

- Top marginal corporate income tax rate reduced from 35% to 21%

While the tax form effective date for these provisions is 2018, they are all set to expire and revert to 2017 law after 2025, although the reduction in the corporate tax rate from 35% to 21% is permanent.

Which Provisions Go into Effect in Tax Year 2019?

For some provisions, the answer to the question “when does tax reform start” is not until tax year 2019. Keep an eye out for these provisions that include:

- Elimination of the shared responsibility payment (a.k.a. the individual mandate),

- Elimination of the deduction for payment of alimony pursuant to an agreement entered into after December 31, 2018

- Elimination of the inclusion for alimony received pursuant to an agreement entered into after December 31, 2018

To find out how tax reform effective dates affect your tax filing, visit an H&R Block office and speak with a tax pro in your neighborhood. You can also visit our online tax calculator to see how these changes may affect your refund.

Was this topic helpful?