New Tax Brackets (Tables): What’s Changed With Tax Reform

Editor’s note: This post outlines how the tax brackets changed with tax reform. To find updated tax bracket information, review our “What are the tax brackets?” post.

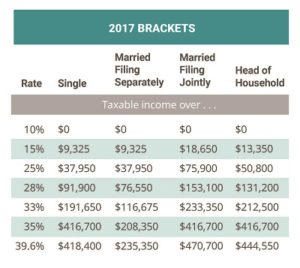

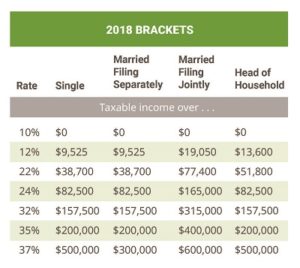

The Tax Cuts and Job Act contains hundreds of changes that affect taxable income, including new tax brackets. To compare the old and new information, view the 2017 and 2018 tax tables below. For additional context, read on and we’ll give you an outline of the new tax brackets and what you need to know.

Note: the brackets for Qualifying Widow(ers) are the same as for Married Filing Jointly Status.

2018 Tax Brackets – What’s the Same

To understand what’s new for the 2018 tax brackets and in the years beyond, it’s helpful to start out with what has not changed. U.S. taxes are still based on a “progressive” system, which means your tax rate increases as your taxable income amount increases. Said differently, only the income that falls in a given range is taxed at that corresponding tax rate.

Keep in mind, taxable income is the basis for the values in the tables above. It is calculated as gross income, less any adjustments, less either the sum of itemized deductions or the standard deduction, whichever is larger.

Tax Reform Brackets – What’s Different

What has changed is that the actual numbers inside of those ranges are now different as are the marginal rates. In general, the tax brackets for 2018 and beyond are slightly broader, and the rates are slightly lower, except for the lowest tax bracket (see marginal tax rates in charts above). The new tax tables for 2018 reflect these changes. According to H&R Block’s analysis of the Tax Cuts and Jobs Act (TCJA), the new tax brackets mean that most taxpayers will pay less tax.

Under the new law, Jessica’s taxable income of $29,350 places her in the 12% tax bracket. She will pay:

- 10% on the first $9,525 of taxable income ($9,525 x 10% = $952)

- 12% on the amount over $9,525 ($19,825 x 12% = $2,379)

By adding the amounts for each segment, $952 + $2,379, we see her federal tax for 2018 will be $3,331.

Under the previous law, Jessica’s taxable income of $29,350 would have placed her in the 15% tax bracket. She would have paid:

- 10% on the first $9,325 of taxable income ($9,325 x 10% = $932)

- 15% on the amount over $9,325 ($20,025 x 15% = $3,003)

By adding the amounts for each segment, $932 + $3,003, we see her federal tax would have been $3,935, or $604 higher.

It’s important to keep in mind that Jessica’s lower tax under the TCJA is not just due to the new tax brackets. The 2018 tax tables reflect the bracket changes and a combination of three other elements:

- a higher new standard deduction ($12,000 under the TCJA vs. $6,350 under previous law)

- the loss of a personal exemption under the TCJA ($4,050 under previous law) and

- the reduction in tax rate.

Have Questions About the New Tax Brackets?

If you need help understanding how the new tax brackets or tax reform impacts you, our knowledgeable and friendly Tax Pros can help.

Make an Appointment to speak with a Tax Pro today.

Was this topic helpful?